Share

Published on

The strengh of Buy-Side Trading

With over $17 trillion in global assets under management1 and projected growth towards $30 trillion by 20302 , ETFs have become a rapidly growing asset class, allowing for direct exposure, diversification in the allocation (across asset classes, geography, sectors, etc.), and hedging. In the United States, 2025 saw a historic first: the number of locally listed ETFs now exceeds the number of publicly listed American companies3!

Beyond their growth over traditional underlying asset classes, ETFs are increasingly allowing for active exposure to flexible, sectoral, regional, thematic strategies, or even to less liquid assets.

Source: Bloomberg, Nov 2025

However, the market depth of these instruments, accessible to a wide range of investors, does not reflect the entirety of the liquidity available in the market. This is precisely where a buy-side trading desk - such as Natixis TradEx Solutions (NTEX) - plays a central role by optimizing ETF trading.

ETF is certainly a fund, but more importantly, a listed one.

The Key Expertise of the Trader in the Value Chain

This expertise is characterized at various key moments.

i) ETF trading strategies

The choice between different execution strategies depends on the specific objectives and constraints of each investor (management constraints, order size, liquidity of the ETF being traded, for example). For instance, executing at NAV offers predictability and stability for the investor, as it is based on the actual value of the underlying assets and calculated after market close, also limiting market impact for large transactions or less liquid ETFs; on the other hand, market execution offers more flexibility, allowing the trader to seize live market opportunities (premium/discount relative to the ETF's indicative NAV).

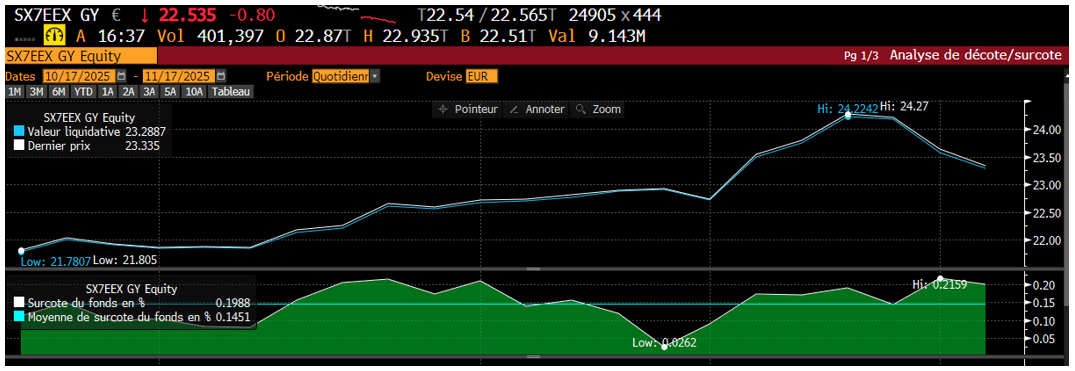

Example 1 : iShares Euro Stoxx Banks - SX7EEEX GY - listing Xetra (Germany):

Source: Bloomberg, Nov 2025. Past performance is not indicative of future results. References to specific securities, sectors, or markets in this document do not constitute investment advice or recommendations.

In this specific case of a banking ETF, we observe a “premium” in the market of 15 bps over its indicative NAV (or fair value) over a one-month period.

A buyer during this period could have opted for an execution at NAV to seek to limit the impact of this premium in the execution.

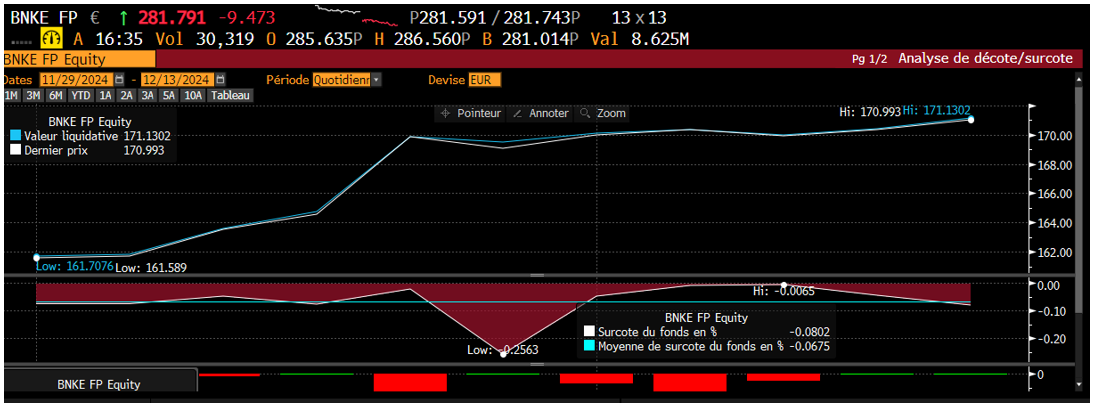

Example 2 : Amundi Euro Stoxx Banks - BNKE FP - Listing Paris (France):

Source: Bloomberg, Nov 2025. Past performance is not indicative of future results. References to specific securities, sectors, or markets in this document do not constitute investment advice or recommendations.

In this second case, and over another ETF on the banking sector, we observe a discount in the market of 7 bps relative to its indicative NAV over a short period (29/11 – 13/12). A buyer during this period could have chosen to execute at market to take advantage of the market opportunity during execution.

Thus, we have observed in these two scenarios, within the same sector, an interest in buying the ETF at market or at NAV depending on the prevailing market conditions at the time of execution.

In the case of an execution at NAV (primary process of creation/redemption of shares), the trader can check prerequisites, such as size, versus the minimum required by ETF issuers or ensure that the various markets listing the stock basket inside the ETF are open, or that cut-offs corresponding to the deadlines for creation/redemption are met. Then, they proceed with trading and liquidity sourcing.

In the case of an execution at market, the trader performs a pre-trade analysis to ensure that the instrument can be executed under the best market conditions using the tools and metrics at their disposal (including those from electronic trading), enabling him to have an instant view of:

- Active market participants on the ETF in question

- Available interests/axes

- Execution statistics per each broker (hit ratio, response rate)

Buy-side trading aims to increase sources of liquidity from different types of market participants—market makers, banks, brokers—seeking to reduce market impact and exploit competitive spreads, particularly through requests for quotes (RFQs ), thereby providing access to hidden liquidity while putting brokers in competition.

Based on this assessment, the trader can suggest the most efficient execution strategy (e.g., selling an ETF at NAV when it trades at a discount in the market; or selling an ETF at market when it trades at a premium).

ii) Choosing the Trading Venue Based on the Listing Exchange

The buy-side trading team also brings its expertise during an investor's decision-making process. Indeed, these instruments can be registered and listed on multiple exchanges, with different characteristics: codes, currency... This sometimes brings added complications to the ETF market, making the contribution of trading (a broad perspective) essential. For instance, based on liquidity or exposure to currency risk, it may be appropriate to invest on one exchange rather than another.

For example, an ETF on the underlying Gold commodity will trade on the Paris exchange in Euro and on the Amsterdam exchange in USD.

Innovate and improving processes

In light of increasing volume being traded on this asset class, NTEX continuously enhances its operational efficiency by integrating innovative solutions to optimize the trading process.

Regular discussions on execution strategies and listing venues occur with clients. To meet new client needs, NTEX has also deployed an execution process capable of absorbing significantly increased volumes: after defining execution rules and constraints thanks to its knowledge of execution channels and strategies, it is possible to address requests in a semi-automated way for certain identified orders with the aim to improve execution quality.

In addition, NTEX relies on its work around data to enhance its effectiveness regarding ETFs by deepening its search of liquidity and best price. NTEX is actively working on improving its broker recommendation tool for pre-trade, similar to what is done on other asset classes. This initiative aims to provide the trader with recommendations, in addition to other market information, based on NTEX’ past executed orders (post-trade) on ETFs in particular.

In conclusion, in a constantly expanding market, buy-side trading is an essential link in the value chain of ETF execution, through its assessment of market conditions, its ability to access implicit liquidity, and the optimization of execution by choosing the appropriate channel.

Laurent Albert

Deputy CEO, Global Head of Execution

Mallé Siby

Equity, ETF & Derivatives Trader

(1) Global ETF assets hit record $17.85tn at August-end https://funds-europe.com/global-etf-assets-hit-record-17-85tn-at-august-end/

(2) ETFs 2029: The path to $30 trillion https://www.pwc.com/gx/en/industries/financial-services/publications/etf-survey.html

(3) There Are Now More ETFs in US Than There Are Individual Stocks https://www.bloomberg.com/news/articles/2025-08-25/us-etfs-eclipse-total-number-of-stocks-in-paradox-of-choice-for-investors

(4) RFQ : Request for quotation : demande de prix aux contreparties en vue de les mettre en concurrence

This newsletter is exclusively for professional clients as defined by MIFID; its content does not constitute an invitation, advice, or recommendation to subscribe, acquire, or dispose of financial instruments. The services mentioned do not take account of any investment objective, financial situation, or specific need of any recipient of this newsletter. NTEX cannot be held responsible for financial losses or any decisions made based on information in this presentation and does not provide any advisory or recommendation services, particularly in terms of investment services.